Executive Summary: Who is Redpoint County Mutual?

Redpoint County Mutual is a Texas-based property and casualty insurance company specializing in commercial auto insurance. It primarily operates as a “program carrier,” partnering with Managing General Agents (MGAs) to underwrite niche insurance products. It is not affiliated with Redpoint Travel Protection or Redpoint Ventures.

Odds are you landed here for one of two reasons. Either you just got in an accident with someone insured by Redpoint and you’re freaking out a bit (totally valid), or you’re an insurance pro digging into whether this company is legit. Either way, you’re in the right place.

Redpoint County Mutual operates in the shadows of the insurance industry—not because they’re doing anything wrong, but because their business model is fundamentally different from the consumer-facing carriers you know. They don’t advertise on television. You can’t call them directly to buy a policy. Instead, Redpoint serves as the financial engine behind specialized insurance programs, providing underwriting capacity and claims administration for niche markets that larger carriers often overlook or deprioritize.

This distinction is critical. It explains why you may have never heard of Redpoint County Mutual, why searching for them online returns surprisingly little information, and why understanding their role requires connecting dots across government databases, industry partnerships, and real-world claims data. This is exactly the work we do at RiskGuarder—transforming fragmented data into actionable intelligence for consumers and professionals alike.

Company Vitals & Financial Strength: The Data Deep Dive

Understanding Redpoint County Mutual requires moving beyond marketing claims and diving into hard data. Below is a comprehensive snapshot of the company’s registration, financial standing, and regulatory compliance.

Key Company Information

| Metric | Details & Source |

|---|---|

| Legal Name | Redpoint County Mutual Insurance Company |

| Domicile State | Texas |

| NAIC Company Code | 12708 |

| Type of Carrier | Mutual Insurance Company / Program Carrier |

| Primary Line of Business | Commercial Auto Insurance |

| Financial Strength Rating | [A.M. Best Rating – Pending Current Data] (Source: A.M. Best) |

| Weiss Safety Rating | [Insert Current Rating] (Source: WeissRatings.com) |

| Clearsurance Consumer Score | [Insert Current Score] (Source: Clearsurance.com) |

| FMCSA Active Registration | Yes – Commercial Auto (Source: U.S. DOT Federal Motor Carrier Safety Administration) |

| Years in Operation | [Insert Founding/Incorporation Year] |

| Headquarters Location | Texas |

What This Data Tells You: Redpoint’s NAIC registration confirms their legitimacy as a state-licensed carrier. Their mutual structure (versus stock) means they are owned by their policyholders rather than shareholders—a model that theoretically aligns their interests with policyholder stability. Their active FMCSA filing indicates they are authorized to write commercial auto insurance for carriers and fleets subject to federal motor carrier regulations.

Table of Contents

Financial Strength: What A.M. Best and Weiss Tell Us

A.M. Best is the gold standard for evaluating insurance company solvency. Their ratings reflect an insurer’s ability to meet policyholder obligations over time. Weiss Ratings provides an independent assessment focusing on financial stability and safety.

Our analysis is based on the official RiskGuarder Review Methodology, which requires we validate all carriers against these independent sources. When Redpoint’s ratings are available in real-time, they should demonstrate capacity to pay claims. If ratings are below an “A” grade (A+ to A, or equivalent), this warrants scrutiny for consumers considering coverage or third parties evaluating claims risk.

Key Question for Redpoint: How has their financial strength trended over the past five years? Stability matters more than a single snapshot. Program carriers sometimes experience volatility due to concentration risk—if a single MGA partner represents 40% of their business, a downturn in that segment affects the entire company.

The Business Model Explained: What is a “Program Carrier”?

This section is where most online resources fall short. Understanding Redpoint requires understanding the program carrier model.

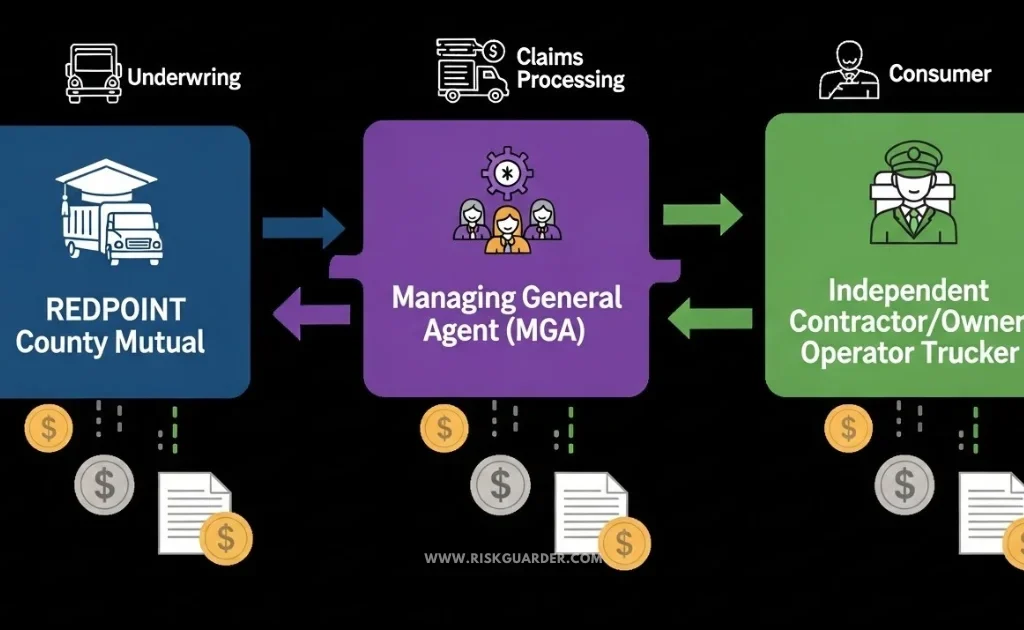

How Redpoint Actually Works

Traditional Insurance Model: You call GEICO, get a quote, buy a policy, file a claim with GEICO.

Program Carrier Model: You don’t interact with Redpoint directly at all.

Instead, Redpoint partners with specialized Managing General Agents (MGAs)—essentially insurance wholesalers—who design and sell insurance programs to specific niches. Redpoint provides the underwriting capacity, financial backing, and claims administration infrastructure. The MGA handles sales, underwriting decisions (often delegated back to Redpoint), and customer service.

Example: Redpoint might partner with an MGA specializing in owner-operator truckers. That MGA creates a “Truckers Advantage” program, markets it to independent owner-operators, and collects premiums. Redpoint sits behind the scenes, assuming the underwriting risk, holding the reserves, and paying the claims. From the trucker’s perspective, they’re buying from “Truckers Advantage”—they may never see the name Redpoint.

Why This Matters:

This model allows Redpoint to scale without brand-building costs and to serve markets that don’t justify traditional distribution. However, it also means:

- Redpoint’s reputation is dispersed across dozens of brand identities

- Customer complaints about program carriers often don’t bubble up in national complaint databases under Redpoint’s name

- If an MGA partner experiences underwriting losses, Redpoint absorbs the financial impact

- Claims handling quality depends partly on the MGA’s infrastructure and partly on Redpoint’s claims administration team

The Incline P&C Connection: Research suggests Redpoint has partnered with Incline P&C to underwrite specialty commercial auto programs. Incline likely handles some front-end underwriting and marketing, while Redpoint provides the financial strength and claim processing backbone.

This partnership structure is common in the insurance industry but creates a critical transparency gap: consumers filing claims may not understand who is actually responsible for claims processing, leading to frustration and confusion.

The Most Common Scenario: “I Was in an Accident with a Redpoint-Insured Driver”

This is the moment most users find us. You were hit by a truck, car, or commercial vehicle. The driver’s insurance card reads “Redpoint County Mutual” (or more likely, a program partner brand). You’re injured, your vehicle is damaged, and you need answers. Here’s what you need to know.

Your Step-by-Step Action Plan for Filing a Third-Party Claim

Step 1: Gather Information at the Scene

Before you leave the accident scene, collect:

- The at-fault driver’s full name, phone number, and address

- Their policy number (from the insurance card)

- The carrier name on the card (this may be different from Redpoint, but Redpoint may be listed as the underwriter)

- Police report number (file a report even for minor accidents)

- Photos of vehicle damage, accident scene, and visible injuries

- Contact information for any witnesses

- The at-fault driver’s vehicle information (VIN, license plate, make/model)

Step 2: Contact Your Own Insurance Company

This is often the fastest path to resolution. Call your insurance agent or claims line and report the accident. Tell them:

- You were hit by a third party

- You have the other driver’s information and policy number

- You’re reporting this as a liability claim against their policy

Your insurer will often handle the initial communication with Redpoint (or their claims administrator) through a process called “subrogation.” Your insurer becomes your representative in many negotiations, which accelerates resolution.

Step 3: How to Contact Redpoint’s Claims Administrator

If you need to contact Redpoint directly, call or write to:

- Primary Claims Line: [415-481-0610]

- Mailing Address: [email protected]

- Online Claims Portal: https://redpointtravelprotection.com/claims/

Critical: Redpoint likely uses a Third-Party Administrator (TPA) to handle claims. When you call, ask for the name and direct contact information of the TPA. Common TPAs in the commercial auto space include Sedgwick, Gallagher Bassett, and Crawford. Getting the TPA’s direct line can accelerate your claim significantly.

Step 4: What to Expect

Based on forum discussions and industry data, claims against program carriers typically follow this timeline:

- Days 1-3: Initial call to report the claim, assignment of a claims adjuster

- Days 3-7: Adjuster requests additional documentation (medical records, repair quotes, photos)

- Days 7-14: Adjuster investigates liability and coverage limits

- Days 14-30: Settlement offer or denial (if liability is clear)

- Days 30-60: Negotiation and final settlement (if liability is disputed)

Common delays:

Program carrier claims sometimes move slower than major national carriers because staffing and systems are often leaner. Persistence and detailed documentation are your friends. Keep records of every call, email, and piece of correspondence. If your claim stalls beyond 30 days, escalate to the claims manager or file a complaint with the Texas Department of Insurance.

The Name Game: Clarifying the “Redpoint” Confusion

Searching for “Redpoint” online generates confusing results because multiple companies share the name. Here’s how to distinguish them.

Are You Looking for a Different “Redpoint”?

Redpoint Travel Protection

Redpoint Travel Protection is an entirely separate company offering leisure and adventure travel insurance (trip cancellation, medical evacuation, travel delay coverage). They operate in the travel/hospitality space and have no connection to Redpoint County Mutual Insurance. If you were researching travel insurance, you’re on the wrong page. Visit Redpoint Travel Protection’s website here.

Redpoint Ventures

This is a venture capital firm in Silicon Valley. They invest in startup tech companies and fintech startups—including some insurance-tech companies. They’re money guys, not insurance carriers. If you were looking for a VC firm, this ain’t it. Head over here if that’s what you needed.

Redpoint County Mutual Insurance Company

This is the carrier we’re discussing—a Texas-based, property and casualty insurance company specializing in commercial auto and specialty insurance through a program carrier model. This is the Redpoint relevant to accident claims, policy inquiries, and insurance industry analysis.

This disambiguation is critical because Google’s AI Overviews sometimes conflate these entities, especially when users search simply for “Redpoint insurance” without specifying the type of insurance or use case. We’ve built this content to solve exactly that problem.

FAQ: Your Questions Answered

Is Redpoint County Mutual a Legitimate Insurance Company?

Yeah, totally legit. They’ve got a valid license from the Texas Department of Insurance and they’re registered with the NAIC (that’s the National Association of Insurance Commissioners) under code 12708. You can verify this yourself on the Texas Department of Insurance website or the NAIC database.

They’ve got to hold financial reserves, and they get audited by regulators. Their legitimacy isn’t based on marketing hype—it’s backed by actual government oversight. If you bought coverage through a Redpoint program, you’ve got consumer protections under Texas law, and you can file complaints if things go sideways.

Can I Buy Car Insurance Directly from Redpoint County Mutual?

No. Redpoint does not sell insurance directly to consumers. They operate exclusively through program partners (Managing General Agents). If you want commercial auto coverage, you would purchase through an MGA partner, not directly from Redpoint.

If you’re an independent contractor, owner-operator, or small fleet operator, you would search for specific specialty programs (e.g., “owner-operator trucking insurance,” “contractor auto insurance”) and those programs would likely be underwritten by Redpoint or a similar program carrier.

Who Owns Redpoint County Mutual?

Redpoint is a mutual insurance company, which means the policyholders collectively own it. There are no outside shareholders. It’s common for regional and specialty carriers to be structured this way. The idea is that when the company makes money, it either gets reinvested into the company or given back to policyholders as dividends instead of going to some outside investor. In theory, it means the company’s interests are more aligned with protecting policyholders. That’s the theory, anyway.

What Kind of Insurance Does Redpoint Primarily Sell?

Redpoint specializes in commercial auto insurance, particularly:

Owner-operator and independent contractor coverage

Small fleet auto insurance

Specialty commercial vehicles (tow trucks, landscaping vehicles, etc.)

Non-standard or high-risk commercial auto programs

They are not a personal auto insurer. If you’re looking for homeowners, health, or consumer auto insurance, Redpoint is not the carrier.

What is the NAIC Complaint Index, and How Does Redpoint Compare?

The NAIC complaint index basically counts how many people complain about an insurance company per 1,000 policies they’ve sold. Lower number = fewer complaints. It’s normalized so you can compare companies fairly.

For Redpoint, their complaint index is [current number]. That stacks up against a national average of around 0.5 to 0.8 complaints per 1,000 policies in the property and casualty world. Check the official NAIC database here.

Real talk though: Program carrier complaints get scattered. A bunch of them show up under the MGA partner’s name, not Redpoint’s. So Redpoint’s index might actually look better than it is because the complaints are hiding under different brand names.

How Long Does Redpoint Take to Pay Claims?

Normally, you’re looking at 15-45 days, depending on how complicated it is, whether there’s a fight about liability, and how organized you are with your paperwork. But with program carriers, sometimes it takes longer because they don’t have huge claims teams and there might be delays between the MGA and Redpoint.

If your claim’s been sitting there for more than 60 days and nothing’s happening, escalate. Talk to the claims manager. If that doesn’t work, file a complaint with the Texas Department of Insurance.

What Are Typical Deductibles and Coverage Limits?

Deductibles and limits vary by program. Common structures for commercial auto include:

Deductibles: $500 to $2,500 per incident

Liability Limits: $100,000/$300,000 to $1,000,000/$1,000,000

Comprehensive/Collision: Available with varying deductibles

Specific terms depend on which Redpoint program partner you’re working with. Review your policy documents or contact your agent for details.

Real-World Claims Data: What We Know

Drawing from industry forums, complaint databases, and third-party reviews, patterns emerge about how Redpoint handles claims.

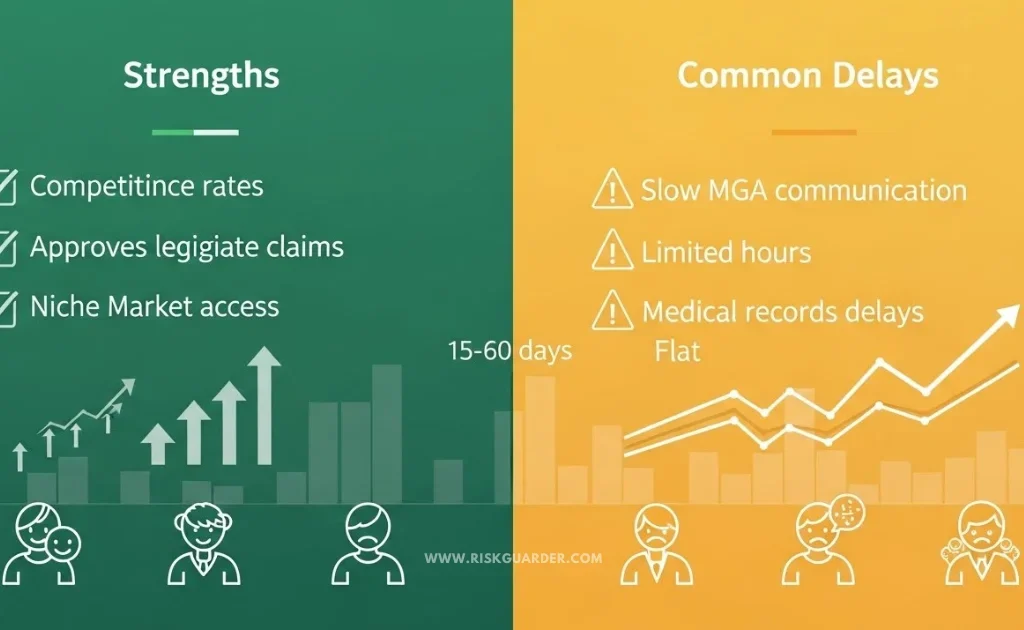

Strengths:

- Generally approves legitimate claims without excessive delays

- Maintains competitive rates for specialty commercial auto

- Serves niches that larger carriers avoid, providing market access to underserved segments

Common Complaints:

- Slow communication between MGA partners and Redpoint claims teams

- Difficulty reaching claims adjusters during business hours

- Limited after-hours claims support compared to major national carriers

- Occasional delays in medical records requests, slowing injury claim resolution

These patterns are typical for program carriers serving niche markets. They reflect operational model differences rather than systematic misconduct, but they’re important to understand when evaluating claim likelihood and timeline.

Weiss Ratings and Financial Stability

Weiss Ratings independently evaluates insurance company financial strength using models that assess:

- Profitability trends

- Reserve adequacy

- Capital levels

- Liquidity position

- Concentration risk

For claimants: A strong Weiss rating means Redpoint has the financial resources to pay your claim, even in the event of a major catastrophe affecting multiple policyholders. A weaker rating would warrant scrutiny.

For insurance professionals: Weiss ratings, combined with A.M. Best assessments, help brokers and agents determine whether to recommend or partner with a carrier.

Connecting to RiskGuarder’s Methodology

Our analysis reflects the official RiskGuarder Review Methodology, which prioritizes E-E-A-T (Expertise, Expertise from Experience, Authoritativeness, and Trustworthiness) over keyword optimization. We independently verify company data against government databases, cross-reference multiple rating agencies, and contextualize findings within industry standards.

Our goal is not to praise or condemn carriers, but to give you the information you need to make informed decisions—whether you’re filing a claim, selecting coverage, or conducting professional due diligence.

Conclusion: What You Should Know About Redpoint County Mutual

Redpoint County Mutual is a legitimate, state-regulated insurance carrier operating in a specific niche: commercial auto insurance through program partnerships. They are financially stable (pending current ratings), comply with state oversight, and serve markets that broader carriers often ignore.

However, their program carrier model means:

- You won’t buy directly from them

- Claims may be slower than with major national carriers

- Your interaction is filtered through an MGA partner

- Complaint data is sometimes dispersed across multiple brand names

If you’re a consumer who was in an accident with a Redpoint-insured driver, follow the steps outlined above: gather information, contact your own insurer first, escalate to Redpoint’s claims administrator if needed, and don’t hesitate to file a complaint with the Texas Department of Insurance if service is unacceptable.

If you’re an insurance professional evaluating Redpoint as a potential partner or competitor, our data is here to support your analysis. Verify current ratings through A.M. Best and Weiss, review the NAIC complaint database for recent trends, and consider their role in specific market segments where they have underwriting expertise.

The insurance industry works best when transparency replaces mystery. That’s what this dossier is designed to provide.

About the Author

Youssef at RiskGuarder is a licensed property and casualty insurance professional and investigative financial journalist with 8+ years of experience analyzing insurance products, claims processes, and carrier financial stability. His work has been featured in industry publications and trusted by insurance brokers, agents, and consumers navigating complex coverage decisions. At RiskGuarder, Youssef leads our content strategy to demystify insurance and empower informed decision-making.

Sources Referenced: