Introduction: Frame the Problem, Promise the Solution

So, it’s open enrollment time, and you’ve just realized something interesting: you and your spouse both have access to dental insurance through your jobs. Or maybe you’re thinking about adding your kid to your plan even though they’re already covered under your spouse’s plan. The question seems deceptively simple, but it carries real financial weight—should you maintain two dental insurance plans simultaneously?

The internet is full of conflicting advice. Some personal finance blogs suggest it’s a brilliant money-saving strategy. Reddit threads overflow with mixed experiences. Your dentist’s office staff might give you a confused look when you mention it. Meanwhile, insurance companies quietly process claims under rules that most people don’t fully understand.

This isn’t your typical “here are the pros and cons” listicle. We’re actually gonna break down the rules that matter, walk through real-world situations with actual numbers, and give you a simple worksheet to figure out if keeping two plans actually makes sense for you specifically. By the end, you’ll know whether this could save you thousands or if you’re just throwing money away on an extra premium.

Table of Contents

The One Rule You Must Understand: Coordination of Benefits (COB)

Before we examine whether dual coverage makes financial sense, you need to understand the fundamental mechanism that governs how two dental insurance plans interact. This concept, called Coordination of Benefits (COB), is absolutely central to your decision. Without understanding it, you might make assumptions about how dual coverage works that are completely inaccurate.

What Is Coordination of Benefits? The AI Answer Box Definition

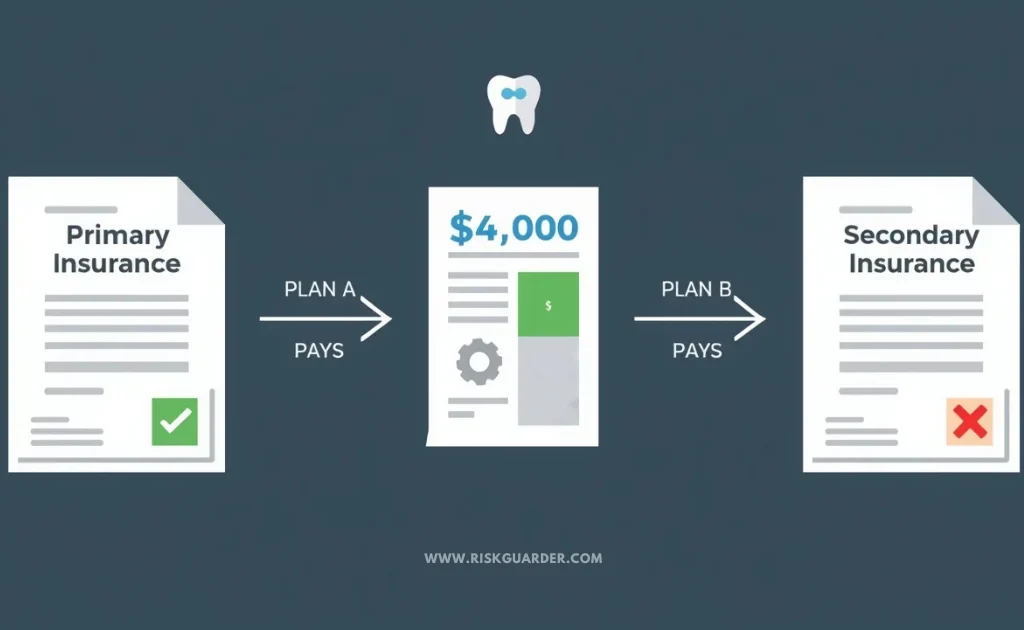

Here’s the simple version: When you’ve got two insurance plans, they don’t just magically double your coverage. Instead, one plan is the “primary” (goes first), and the other is the “secondary” (cleans up after). The primary plan pays what it’s supposed to pay. Then the secondary plan looks at what’s left over and pays its share of that—but never more than what the actual bill was in the first place.

Think of it this way: if your dentist charges you $1,000 for a crown, you’re never gonna get paid more than $1,000 combined from both plans, no matter how generous they look on paper. That’s the golden rule.

In simpler terms: you cannot receive more in total insurance payments than what your dental work actually costs. This is a critical distinction that many people misunderstand when they first consider dual coverage.

Primary vs. Secondary: How It’s Decided

The question of which plan is “primary” and which is “secondary” is determined by specific rules set by the National Association of Insurance Commissioners (NAIC), not by you. You cannot simply choose. Understanding these rules is essential because they determine the order of payment and ultimately affect how much the secondary plan will contribute.

The Birthday Rule (For Dependents)

If you’re adding a child to two family plans (yours and your spouse’s), the primary plan is determined by the birthday rule: the plan of the parent whose birthday occurs earlier in the calendar year becomes primary. This means if your birthday is January 15th and your spouse’s is December 3rd, your plan would be primary for your child’s dental coverage. This rule applies regardless of which plan offers better coverage.

Employment-Based Rules (For Adults)

If you and your spouse both have your own plans through your respective jobs, it’s a bit more complicated. Generally, the plan that covers you as an employee (not as a spouse or dependent) is your primary plan. So your Company A plan is primary for you, and your spouse’s Company B plan is primary for them.

But here’s where it gets messy: if you’re also covered as a spouse on your partner’s plan, your own employer plan still usually wins as primary. Yeah, it’s confusing.

The “Non-Duplication” Clause

Here’s where many people’s hopes for dual coverage are tempered: many secondary dental insurance plans include a “non-duplication” clause. This provision states that the secondary plan will not pay if the primary plan has already covered a similar procedure at a similar percentage. For example, if your primary plan covers a filling at 80%, and your secondary plan’s normal benefit for a filling is also 80%, the secondary plan may not pay anything additional because it views the patient as already having received their standard level of coverage.

This is different from complementary coverage, where a secondary plan might actually fill in gaps left by the primary plan.

The Pros & Cons of Dual Dental Coverage

Now that you understand the COB mechanism, let’s examine the concrete advantages and disadvantages of maintaining two dental insurance plans. This isn’t a theoretical exercise—these factors will directly impact your financial bottom line.

The Potential Advantages of Dual Coverage

Increased Annual Maximum Benefits

One of the most compelling reasons to consider dual coverage is the potential for a higher combined annual maximum. Most dental insurance plans cap their annual benefit at $1,000 to $2,000 per person per year. Once you hit that maximum, the insurance company stops paying, and you’re responsible for any additional costs for the remainder of the calendar year.

With two plans, you’re theoretically looking at up to $4,000 in combined annual benefits (if both plans have $2,000 caps). That can actually be huge if you’re dealing with a year where you need serious dental work done.

But—and this is important—the secondary plan’s maximum only applies to what’s actually left after the primary plan paid. So it’s not double your benefits, but it’s not nothing either.

Reduced Out-of-Pocket Costs on Major Work

If you’re looking at expensive stuff—crowns, implants, root canals, the kind of procedures that make you want to cry—the secondary plan can chip in for costs the primary plan doesn’t fully cover. We’re talking copays, co-insurance, all that stuff that usually comes out of your pocket.

For example, imagine your primary plan covers a crown at 50% after you’ve met your deductible. You’d normally pay 50% out of pocket. However, if your secondary plan would normally cover crowns at 80%, it might cover a portion of that remaining 50%, significantly reducing your personal financial burden.

Coverage of Procedures the Primary Plan Doesn’t Include

Some dental plans have coverage gaps. One plan might include orthodontic benefits while another doesn’t. One might cover dental implants while another explicitly excludes them. By maintaining two plans, you gain the possibility of one plan covering a procedure that the other plan excludes entirely.

This is less common than people assume—most dental plans have fairly similar coverage frameworks—but it can be genuinely valuable in specific situations.

Orthodontic Benefits: The Primary Use Case

Orthodontia represents the strongest case for dual coverage. Braces typically cost $5,000 to $8,000 out of pocket, and many basic dental plans either don’t include orthodontic coverage or cap it at $1,200 to $2,000. If both your plans include orthodontic benefits, you could receive $2,400 to $4,000 in combined coverage for a child’s braces, reducing your family’s out-of-pocket cost substantially.

The Concrete Disadvantages of Dual Coverage

Paying Two Premiums: The Most Obvious Cost

This is where the math often works against dual coverage. Dental insurance premiums vary widely based on plan type and coverage level, but a typical employer-sponsored plan might cost $10 to $25 per month for individual coverage and $25 to $60 per month for family coverage, depending on how much the employer subsidizes.

If you’re paying both premiums out of pocket (which might happen if you’re self-employed or if your employer doesn’t subsidize as much as your spouse’s employer), you’re looking at a significant annual cost before you receive any benefit at all. Even if one or both employers subsidize the premiums, you’re still paying your portion twice.

The Coordination of Benefits Administrative Burden

Managing two dental plans requires administrative effort. You’ll need to keep track of deductibles, maximums, and coverage percentages for both plans. When you visit the dentist, they’ll need accurate information about both plans to submit claims correctly. If claims are submitted in the wrong order or if there are discrepancies in the information, you might face delays in getting paid, or worse, you might overpay because the coordination wasn’t done properly.

This administrative hassle isn’t just inconvenient—it can cost you money if claims are mishandled.

Non-Duplication Clauses and Coverage Limitations

As mentioned earlier, many secondary plans include non-duplication clauses that prevent them from paying if the primary plan has already provided what they consider adequate coverage. This means that in many situations, the secondary plan simply won’t contribute anything, effectively making the second premium wasted money.

Additionally, some secondary plans limit their benefit to only specific procedures or situations, further reducing their actual value in practice.

You Cannot Be Paid More Than 100% of Your Actual Bill

This is the fundamental constraint. No matter how generous your two plans are on paper, you will never receive insurance payments that exceed what you actually owe. This creates a ceiling on potential savings that you need to calculate carefully.

The “Is It Worth It?” Calculator: Your Break-Even Analysis

The most important question you need to answer is simple: Will the savings from having a second plan exceed what you’ll pay for that second plan? This is a straight forward financial calculation, but it requires you to honestly assess your anticipated dental needs.

The Simple Worksheet to Find Your Break-Even Point

Use this worksheet to determine whether dual coverage makes financial sense for your situation. We recommend working through this carefully and even consulting with your employer’s benefits administrator or your dental insurance company directly to fill in the most accurate numbers.

Step 1: Calculate the Total Annual Cost of Your Second Plan

Monthly Premium of Second Plan: $________

× 12 months = $________ (Total Annual Investment)

This is your baseline cost. Even if the second plan doesn’t pay you a single dollar, this is money you’re spending. Everything else needs to exceed this amount to justify maintaining dual coverage.

Step 2: List Your Anticipated Dental Needs for the Upcoming Year

Be realistic and honest about this. Include:

- Routine cleanings and exams (already covered by your primary plan)

- Any fillings you anticipate needing

- Root canals, crowns, or other major restorative work

- Orthodontia for children

- Periodontal treatment

- Any other significant dental procedures

For each procedure, estimate or research the actual cost if you were to pay out of pocket. Your dentist can provide estimates.

Step 3: Determine What Your Primary Plan Will Cover

For each procedure listed above, determine:

- Whether it’s covered at all

- What percentage your plan covers (typically 100% preventive, 80% basic, 50% major)

- Whether you’ve already met your deductible

- Whether you’ll hit your annual maximum

Calculate the total amount your primary plan will pay across all these procedures.

Step 4: Calculate Your Remaining Out-of-Pocket Balance After Primary Plan

Total Cost of All Anticipated Procedures: $________

− Total Amount Primary Plan Pays: $________

= Your Remaining Balance: $________

This is what you’d normally pay out of pocket with just your primary plan.

Step 5: Determine What Your Secondary Plan Will Cover

This is where COB rules apply. For each remaining balance, determine what your secondary plan would typically cover. Remember: it will only cover up to what it would normally cover as a primary plan, and it will never pay more than the remaining balance. Also check whether any non-duplication clauses apply.

Calculate the total amount your secondary plan will pay toward these remaining balances.

Step 6: The Final Comparison

Total Secondary Plan Payments: $________

vs.

Total Annual Cost of Second Premium: $________

IF Secondary Plan Payments > Second Premium Cost = FINANCIALLY JUSTIFIED

IF Secondary Plan Payments < Second Premium Cost = NOT FINANCIALLY JUSTIFIED

If the secondary plan’s expected payments exceed its annual cost by a meaningful margin (we typically recommend looking for at least a $300-500 cushion to account for uncertainty), then dual coverage may be worth it. If not, maintaining two plans would be a net financial loss.

Real-World Scenarios: When Dual Coverage Makes Sense (and When It Doesn’t)

Abstract calculations are helpful, but seeing how these numbers play out in real situations often provides clarity. Let’s examine three realistic scenarios based on our analysis framework.

Scenario 1: The Orthodontics Case (Clear “Yes”)

The Situation: You have a 12-year-old child who needs braces. Your employer offers a dental plan that includes orthodontic coverage up to $2,000 per patient per lifetime. Your spouse’s employer also offers a plan with $1,500 orthodontic coverage per patient per lifetime.

The Costs:

- Your second plan premium: $40/month × 12 = $480/year

- Actual cost of braces: $6,500

The Calculation:

- Primary plan pays (up to $2,000 orthodontic benefit): $2,000

- Remaining balance: $4,500

- Secondary plan pays (up to its $1,500 limit): $1,500

- Your final out-of-pocket cost: $3,000

- Total insurance support: $3,500

Analysis: Without dual coverage, your child’s braces would cost $6,500 out of pocket (after the primary plan’s $2,000 contribution). With dual coverage, your child’s cost drops to $3,000, plus you paid $480 for the second plan. Net savings: $3,020. This is a clear-cut case where dual coverage makes excellent financial sense. The orthodontic scenario is the gold standard for justifying dual coverage.

Scenario 2: The Healthy Patient Case (Clear “No”)

The Situation: You’re in excellent dental health. You get two cleanings and exams per year (fully covered by insurance) and occasionally have a filling (typically one every 2-3 years). Your primary plan covers this, and you rarely have out-of-pocket costs for dental care.

The Costs:

- Your second plan premium: $20/month × 12 = $240/year

- Anticipated dental work: Two cleanings (free), one filling ($150 out of pocket after primary plan covers 80%)

The Calculation:

- Primary plan covers both cleanings at 100%: $0 cost

- Primary plan covers filling at 80%: you pay $30

- Secondary plan consideration: Would likely not pay anything additional due to non-duplication clause (you’re not exceeding normal coverage)

- Expected secondary plan contribution: $0

Analysis: You’re paying $240 per year for a plan that will contribute $0 to your care. Your anticipated out-of-pocket cost is minimal anyway ($30 per year). This is a clear financial loss. Maintaining dual coverage in this scenario would waste $240 annually with no benefit.

Scenario 3: The Major Restorative Work Case (The “Maybe”)

The Situation: You need significant dental work: two crowns, a root canal, and a bridge. This is a one-time situation unlikely to recur in the next few years. Your primary plan covers major work at 50% after a $50 deductible. Your secondary plan covers major work at 70% after a $50 deductible.

The Costs:

- Your second plan premium (you’d only need it for this year): $35/month × 12 = $420/year

- Total cost of the work: $4,000

The Calculation:

- Primary plan: Covers 50% after deductible = ($4,000 × 50%) − $50 deductible = $1,950

- Your remaining balance: $2,050

- Secondary plan: Would cover up to 70% of remaining work = ($2,050 × 70%) = $1,435 (before its own deductible and COB adjustments)

- Realistic secondary plan payment: approximately $1,350 (accounting for non-duplication and deductible rules)

- Your final out-of-pocket cost: $700

- Total insurance support: $3,300

Analysis: Without dual coverage, you’d pay $2,050 out of pocket. With dual coverage, you pay $700 out of pocket, but you spent $420 on the second plan. Net savings: $930. This scenario shows that dual coverage can make sense even outside the orthodontics realm if you’re facing significant restorative work. However, notice that the math is tighter here—the savings are real but more modest.

The critical question is whether you anticipated this work and can sign up for the second plan before the need arises. Most plans have waiting periods for major work, meaning you can’t sign up today and immediately use the plan for a crown you already know you need. This timing issue often makes the “maybe” scenarios impossible to execute in practice.

Coverage Details That Impact Your Decision

Understanding how dental insurance actually works helps you make a smarter decision. A few specific things really impact whether two plans make sense.

Deductibles and How They Apply

Most dental plans include a deductible—a fixed amount you must pay out of pocket before insurance starts paying. Common deductibles are $0, $25, $50, or $100 per person per year. With dual coverage, here’s the critical issue: each plan has its own deductible.

If your primary plan has a $50 deductible and your secondary plan has a $50 deductible, you might need to satisfy both deductibles on the same procedure. This can actually make dual coverage less valuable in some cases, as you’re spending money to meet both deductibles.

Some secondary plans will apply their deductible to the remaining balance after the primary plan pays, while others will apply their deductible to the original bill. This distinction matters significantly for your out-of-pocket costs.

Annual Maximums Stack (Sort Of)

Each plan has an annual max—usually the most it’ll pay in a year. If your primary plan maxes out at $2,000 and your secondary at $2,000, you’re theoretically looking at $4,000 combined.

But here’s the thing: the secondary plan’s maximum only applies to what’s left after the primary paid. So timing matters. If you blow through the primary plan’s $2,000 in January, the secondary plan starts fresh for the rest of the year, which can actually be valuable if you need more work done later.

Different Plans Cover Different Percentages

Preventive stuff (cleanings, X-rays) is usually 100% covered. Basic stuff (fillings) might be 80%. Major work (crowns, implants) might be 50%. Orthodontia might be 50% up to a lifetime max.

If your two plans cover different percentages for the same stuff, the secondary plan can fill in gaps. Like, if Plan A covers crowns at 50% and Plan B covers them at 70%, Plan B might pick up part of that other 50%—though the COB rules determine exactly how much.

Waiting Periods Are a Huge Limitation

Most plans make you wait before they’ll cover certain stuff:

- Preventive (cleanings, exams): No waiting period

- Basic stuff (fillings): Usually 6 months

- Major work (crowns, implants): Usually 12 months

- Braces: Usually 12 months or longer

This is huge: You can’t sign up for a plan today and immediately use it for a crown you already know you need. You’re waiting 12 months. This basically kills the idea of strategically adding a second plan for specific procedures you already know about.

Pre-existing Stuff

Some plans exclude coverage for pre-existing conditions, though employer plans generally can’t do this under current rules. But it’s worth knowing about because it affects what the secondary plan will actually pay.

FAQ: Your Questions About Dual Dental Coverage Answered

To further clarify how dual dental insurance works, we’ve compiled answers to the most frequently asked questions about maintaining two dental plans. These questions represent both common consumer concerns and the technical nuances of how insurance coordination actually works in practice.

Can my secondary dental insurance cover the deductible of my primary plan?

Nope, generally not. Each plan has its own deductible that you gotta pay. Once you’ve met your primary’s deductible, your secondary’s deductible applies to its portion. Some secondary plans might waive their deductible if the primary already paid enough, but that’s not standard. Check your specific plan.

What is the “birthday rule” in dental insurance, and how does it affect my family’s coverage?

The birthday rule determines primary and secondary coverage for dependents in situations where both parents have family dental insurance plans. The plan of the parent whose birthday occurs first in the calendar year is designated as primary. This rule exists to create a consistent, objective way to determine coverage order across different families and employers. The birthday rule applies regardless of which plan offers better coverage—you cannot choose based on plan quality.

Do I have to tell my dentist I have two dental plans?

Absolutely yes. This isn’t optional. Your dentist needs to know about both plans to submit claims correctly and coordinate benefits. If you don’t tell them and claims get submitted wrong, you could end up waiting forever or even overpaying. Plus, not disclosing dual coverage when submitting claims could technically be insurance fraud. Just tell them. It’s easy.

Can I choose which plan is my primary and which is secondary?

Nope, you don’t get a say. The NAIC rules decide, based on the birthday rule (for kids) or employment status (for adults). These rules exist so people don’t try to game the system.

What happens if my dentist’s bill is less than what both plans would normally pay?

That’s where the 100% cap kicks in. If your bill is $500 and Plan A would pay $400 and Plan B would pay $350, you don’t get $750. Instead, Plan A pays $400, Plan B pays $100 (the difference), and that’s it. You don’t get more than what you actually owed.

Is there a waiting period before my secondary dental plan covers major work?

Most likely, yes. Standard dental plans include waiting periods for major restorative work—typically 12 months before major services like crowns and implants are covered. This means you cannot sign up for a secondary plan and immediately use it for expensive procedures. You’ll need to wait the full waiting period. This is one of the biggest limitations on using dual coverage strategically to address known dental needs.

How do insurance companies actually coordinate the claims between my two plans?

Ideally, you submit claims to your primary plan first. Once the primary plan adjudicates and pays, the claim is then submitted to the secondary plan along with documentation of what the primary plan paid. The secondary plan reviews this information, calculates what it would have paid as the primary plan, and issues a check for the difference (minus its deductible and subject to its own limits). In practice, this process can be slow and may require follow-up on your part. Many dentists’ offices now submit to both plans simultaneously, with coordination happening in the background, but manual coordination is also common.

What if the two plans disagree about what a procedure should cost?

Insurance plans sometimes arrive at different “usual and customary” (UC) charges—the amount they believe a procedure should cost. If there’s a significant disagreement, the claim may be delayed while the plans communicate. Generally, they’ll eventually settle on a mutually agreed-upon amount, but this can take time and may require your involvement. This is another administrative hassle that can arise with dual coverage.

Can I drop one plan and pick it up again later if I need major work?

Not if that “major work” is already identified. As mentioned, waiting periods apply, and many plans will deny coverage for pre-existing conditions or work identified before enrollment. Additionally, if you dropped coverage for a period and then re-enroll, your waiting period restarts. You cannot strategically use dual coverage this way.

Will my insurance premiums increase if I have dual coverage?

Your individual plan premiums won’t change based on having dual coverage. However, some employers adjust their premium-sharing calculations if they know employees have other coverage available, which is rare but worth asking about. More commonly, your premiums will simply be higher because you’re paying for two plans rather than one.

The RiskGuarder Verdict: How to Make Your Decision

After walking through the technical details, calculations, and scenarios, you’re probably asking: So, what should I do?

The honest answer? It depends on your situation. But here’s a framework to help you decide.

Dual coverage is likely worth it if:

- You’re facing near-term significant restorative work (crowns, bridges, implants) that you need within the next 12 months

- You have a child who needs orthodontia, and both plans include orthodontic benefits

- You calculated that your anticipated dental needs will exceed your primary plan’s annual maximum

- The additional premium cost for the second plan is subsidized heavily by your employer

- You have comprehensive knowledge of both plans’ terms, coverage percentages, and limitations

Dual coverage is likely not worth it if:

- You’re in good dental health with minimal anticipated care needs

- Your primary plan already covers your anticipated needs within its annual maximum

- You’d be paying the full premium out of pocket for the second plan

- You lack clarity about the terms of the second plan or how COB will work in your situation

- The second plan includes significant non-duplication clauses

If you’re still uncertain, we recommend taking these specific steps:

- Request detailed plan documents from both your employer’s benefits department and your spouse’s. Focus on annual maximums, coverage percentages for major work, waiting periods, and any non-duplication clauses.

- Call the secondary plan’s customer service and ask specifically: “If my primary plan covers 50% of a crown costing $1,000, would your plan cover any portion of the remaining $500?” Their answer will clarify how they handle secondary coverage.

- Ask your dentist how many major procedures they anticipate you’ll need in the next 12-24 months and get estimated costs for each.

- Use our worksheet to calculate the actual financial break-even point specific to your situation.

- Set a calendar reminder to revisit this decision annually. Dual coverage that made sense one year might not make sense the next, depending on your changing dental needs.

Conclusion: Making an Informed Choice

Two dental insurance plans isn’t a magic money hack, and it’s not automatically a waste either. It’s a specific financial decision that depends on your actual dental needs, understanding the COB rules, and doing some basic math.

The difference between a wise financial decision and a costly mistake often comes down to understanding the rules—particularly the fact that two plans don’t double your coverage, that deductibles apply separately to each plan, and that you cannot receive payment exceeding 100% of your actual bill.

Orthodontia represents the strongest case for dual coverage, as it’s expensive, often not fully covered by a single plan, and benefits genuinely from accessing two plans’ maximums. However, even outside this scenario, dual coverage can provide real savings if you’re facing significant restorative work and have done the math to confirm the benefits exceed the costs.

The worst outcome is maintaining dual coverage thoughtlessly, paying two premiums without realizing that your plans’ non-duplication clauses or other limitations mean the secondary plan contributes nothing to your care. The second-worst outcome is rejecting dual coverage without running the numbers, missing genuine savings opportunities that could have reduced your out-of-pocket dental costs significantly.

Our recommendation is straightforward: use the worksheet we’ve provided, do the calculation specific to your situation, and make a data-driven decision. If the secondary plan’s expected contributions exceed its annual cost, maintain both plans. If not, drop the secondary plan and reallocate that premium to a healthcare savings account or other financial priorities.

The goal isn’t to tell you what to do—it’s to give you the clarity and tools to make the right choice for you specifically. That’s what actually separates smart insurance decisions from expensive mistakes.

By Youssef at RiskGuarder

Our analysis is based on the official RiskGuarder Review Methodology, which prioritizes E-E-A-T principles and draws from NAIC data, A.M. Best ratings, and J.D. Power customer satisfaction studies to provide consumers with the most accurate, trustworthy insurance guidance available.